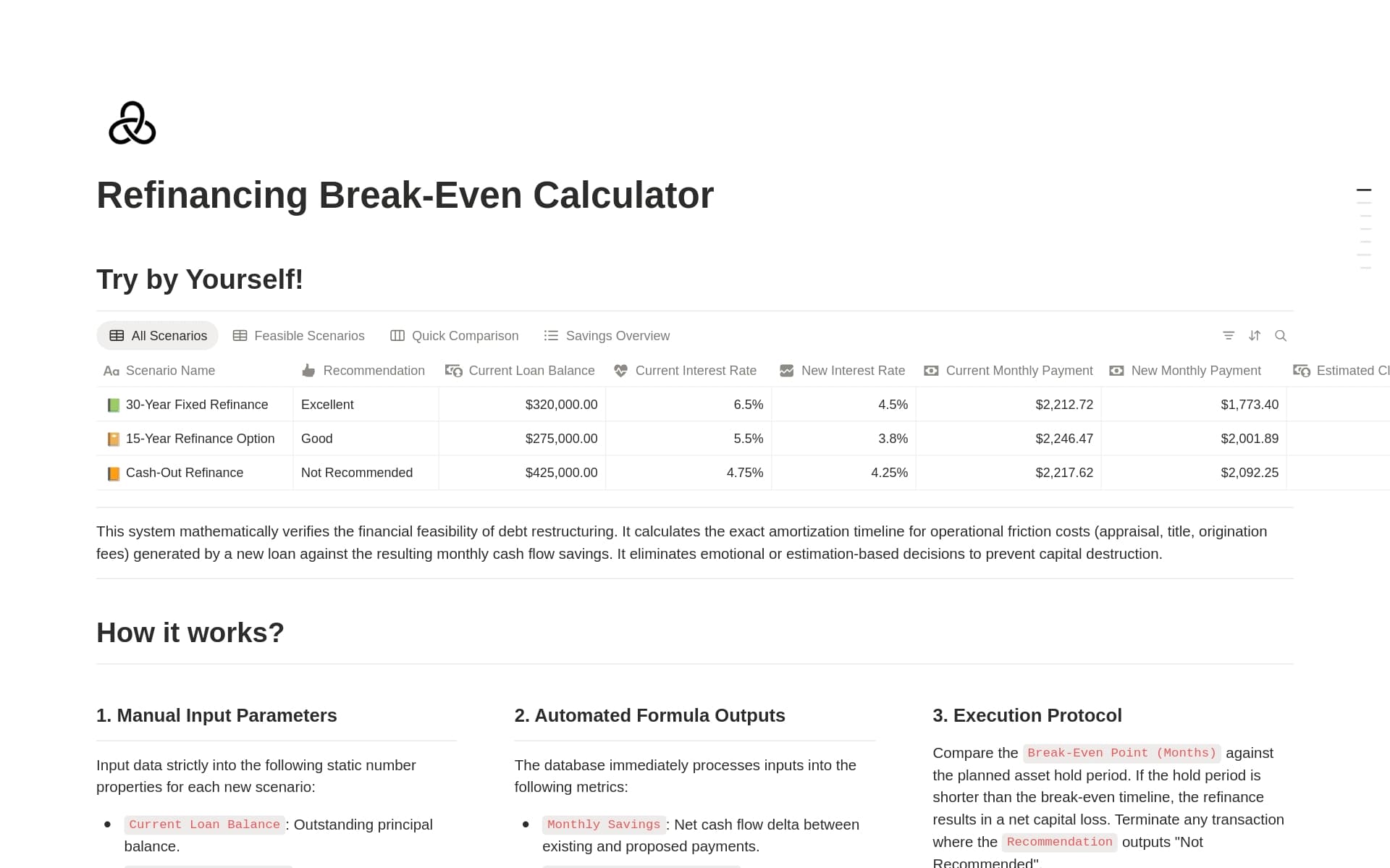

Refinancing Break-Even Calculator

Capital optimization requires ruthless mathematical evaluation, not subjective guesswork based on headline interest rates. The Refinancing Break-Even Calculator provides real estate operators, asset managers, and syndicators with a rigid, formulaic framework to evaluate debt restructuring opportunities. By isolating variables such as interest rate deltas, loan terms, and origination fees, this Notion database prevents value-destroying capital moves and clearly visualizes the exact timeline for profitability.

Rate and Term Analysis

Interest rate reductions do not automatically equate to financial optimization. When evaluating a new term sheet from a lender, operators must weigh the immediate monthly cash flow relief against the long-term cost of resetting the amortization schedule. This module forces users to input their current principal balance, existing interest rate, and remaining term alongside the proposed new loan parameters. The database automatically calculates the delta in monthly debt service, immediately quantifying the gross cash flow increase. By centralizing these metrics, investors can objectively evaluate competing bank term sheets, agency debt, and private syndicate offers against their current debt baseline, stripping away broker sales pitches to expose raw financial utility.

Cost Recapture and Break-Even Velocity

Refinancing generates significant operational friction costs, including third-party appraisal fees, title insurance premiums, lender origination points, environmental reports, and legal counsel retainers. A lower monthly payment is mathematically irrelevant if the holding period of the asset is shorter than the time required to recover these sunk closing costs. The Cost Recapture engine requires users to log every estimated transaction expenditure. The database mathematically divides this total absolute expenditure by the monthly savings delta to output a precise break-even timeline measured in months. If an investor plans to exit a multifamily asset in 24 months, but the calculator output determines the break-even period is 36 months, the system explicitly flags the refinance as a negative-yield action, preventing capital destruction.

Amortization and Cash-Out Tracking

Beyond simple break-even metrics, operators must deeply understand the structural impact on their trapped equity. The system tracks how a new loan term affects principal reduction velocity. Refinancing into a new 30-year term may increase immediate cash flow but will drastically slow down equity accumulation over the hold period. Additionally, for cash-out refinances, the database calculates net proceeds. It deducts the existing loan payoff, all estimated closing costs, and lender-required reserve escrows from the new gross loan amount. This provides the exact liquid capital figure available for subsequent deployment into new acquisitions or required capital expenditures.