Commercial Real Estate Lending OS Architecture

Deal Flow, Underwriting Intelligence, and Portfolio Risk Management.

Commercial real estate lending operates in an environment defined by fragmented information and complex financial risk. A single loan decision may depend on borrower financials, property valuation reports, market conditions, legal compliance, and risk modeling. When these data sources remain disconnected, underwriting becomes slow, inconsistent, and operationally fragile.

A Commercial Real Estate (CRE) Lending Operating System provides structural order to that complexity.

Instead of replacing existing banking systems, a lending OS functions as a strategic visibility layer — a centralized operational framework that organizes deal flow, underwriting intelligence, compliance processes, and portfolio monitoring into a coherent information system.

Platforms such as SectorOps implement this model by structuring commercial lending workflows into connected operational layers.

For more information and other see the other sectors.

Why Commercial Lending Needs an Operating System

Traditional lending workflows often suffer from operational fragmentation:

- Loan documents stored across multiple systems

- Manual coordination between sales, underwriting, and compliance teams

- Inconsistent borrower qualification standards

- Slow underwriting feedback loops

- Limited visibility into portfolio risk exposure

These inefficiencies introduce both decision delays and risk management blind spots.

A lending operating system solves this by transforming lending into structured data flows, where every deal progresses through defined information stages rather than ad-hoc communication.

At a high level, a CRE Lending OS consists of three operational domains:

- Deal acquisition and opportunity tracking

- Underwriting intelligence and risk analysis

- Portfolio monitoring and financial performance visibility

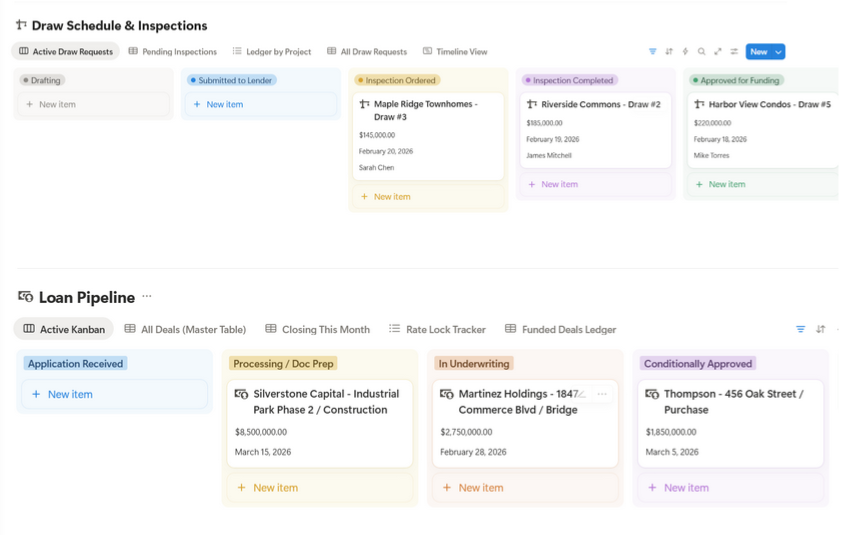

Layer 1: Deal Acquisition System

The acquisition layer manages incoming lending opportunities and borrower relationships.

A structured borrower and deal database allows lenders to track early-stage opportunities with consistent data fields such as:

- Borrower name and entity structure

- Contact information

- Property interest type

- Requested loan amount

- Source of opportunity

Beyond basic information, lenders typically introduce qualification metrics that help evaluate deal quality before full underwriting begins.

Common preliminary indicators include:

- Estimated Debt Service Coverage Ratio (DSCR)

- Target Loan-to-Value (LTV) ratio

- Borrower credit strength

- Property asset type risk

Deals move through a defined pipeline:

- Inquiry

- Pre-qualification

- Documentation collection

- Term sheet issued

- Loan approval

Pipeline visualization significantly improves operational speed because underwriters and deal teams can immediately identify bottlenecks or incomplete documentation.

Layer 2: Underwriting Intelligence System

Underwriting is the analytical core of commercial lending.

Each loan should have a dedicated underwriting workspace where financial analysis, property evaluation, and loan structuring data are organized in a single decision environment.

Borrower Analysis

Underwriters evaluate the financial stability of the borrower by analyzing:

- Financial statements

- Revenue history

- Debt obligations

- Business continuity indicators

This information forms the basis for repayment capacity assessment.

Property Analysis

Commercial real estate loans are heavily dependent on the performance of the underlying asset.

Typical property evaluation data includes:

- Professional appraisal reports

- Market comparables

- Location-specific risk factors

- Occupancy and revenue projections

Combining borrower financial strength with asset performance provides a clearer picture of loan viability.

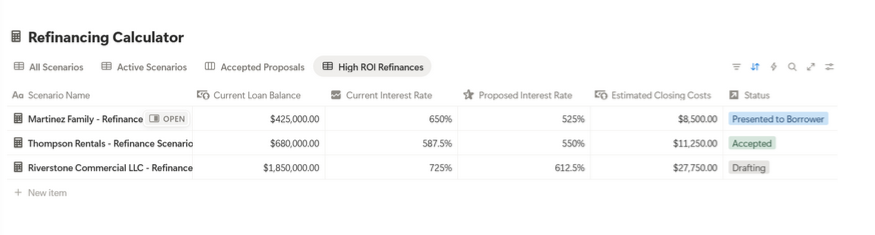

Loan Structuring Data

Once risk analysis is completed, lenders structure the financial terms of the loan:

- Interest rate structure

- Amortization schedule

- Collateral assets

- Guarantee arrangements

By organizing these elements inside a structured workspace, underwriting becomes a repeatable analytical process rather than a manual review scattered across spreadsheets and emails.

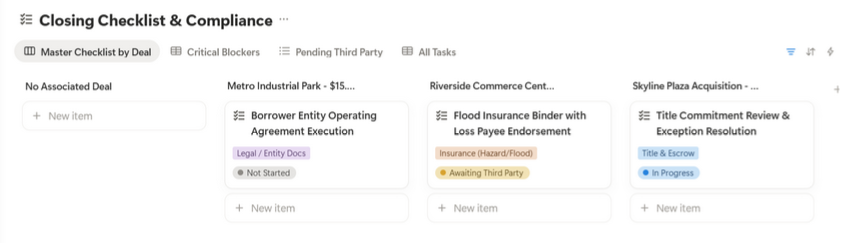

Layer 3: Risk and Compliance Control

Commercial lending is heavily regulated, making compliance monitoring a critical operational layer.

A lending OS must track regulatory documentation alongside financial analysis.

Key compliance checkpoints typically include:

- KYC and AML verification

- Legal contract status

- Insurance verification

- Regulatory filing requirements

Embedding compliance status indicators directly into deal records allows executives to quickly assess regulatory exposure and operational readiness.

Color-coded risk indicators are often used to highlight missing documentation or unresolved legal requirements.

Layer 4: Portfolio Management Dashboard

Once loans are issued, operational focus shifts from underwriting to portfolio monitoring.

Executives need real-time visibility into portfolio health across multiple financial dimensions.

Typical metrics include:

Performance Metrics

- Outstanding principal balance

- Interest income collected

- Payment delinquency status

- Early default indicators

Growth Metrics

- Number of loans originated per month

- Average loan size

- Sector exposure concentration

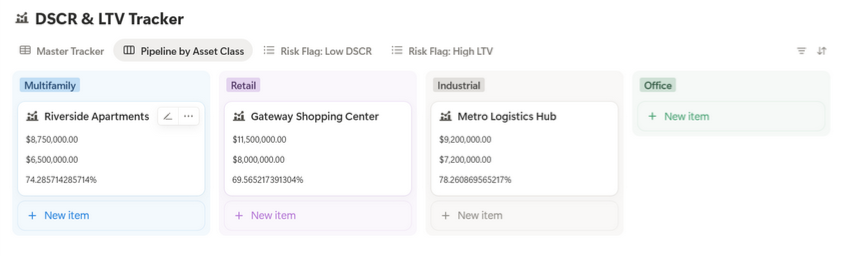

Risk Metrics

- Non-performing loan ratio

- Average portfolio DSCR

- Asset class risk distribution

A centralized dashboard allows leadership teams to evaluate portfolio performance without manually aggregating financial data.

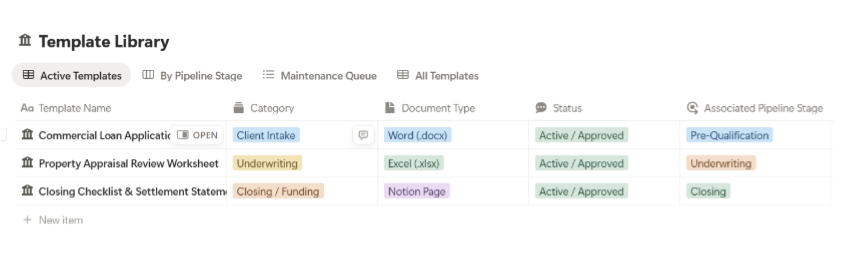

Layer 5: Document Intelligence System

Commercial lending is fundamentally document-intensive.

Loan agreements, property titles, valuation reports, and regulatory approvals must remain accessible and version-controlled.

A document intelligence layer ensures that every loan record maintains a complete legal and financial document history.

This prevents common operational risks such as outdated contract versions, missing legal documentation, or lost appraisal reports.

Layer 6: Workflow Automation

Automation improves efficiency by eliminating repetitive administrative tasks while leaving decision authority with human analysts.

Examples of practical automation include:

- Document request reminders for borrowers

- Loan maturity alerts

- Interest payment reminders

- Compliance renewal notifications

These automated triggers help teams maintain operational discipline without increasing administrative overhead.

Layer 7: Lending Analytics Engine

Advanced lending organizations move beyond descriptive analytics toward predictive risk modeling.

A lending analytics engine can track indicators such as:

- Probability of default scoring

- Historical repayment behavior

- Market cycle sensitivity

- Sector-specific risk models

Data-driven analysis allows lenders to anticipate portfolio volatility before it becomes a financial problem.

Organizational Role Permissions

Because lending data contains sensitive financial information, a well-designed system must implement strict access control.

A typical access hierarchy might include:

- Executives: Portfolio dashboards and risk analytics

- Underwriters: Full deal and financial data access

- Sales teams: Borrower and opportunity data

- Compliance officers: Regulatory and legal records

Segregating access rights protects sensitive financial information while preserving operational collaboration.

Common System Design Mistakes

Several architectural mistakes frequently appear in early lending systems.

Overbuilding Early

Organizations often attempt to implement full analytics and automation before establishing a reliable deal tracking workflow.

Initial focus should remain on deal acquisition and underwriting structure.

Mixing Sales and Risk Data

Acquisition teams optimize for deal flow, while underwriting teams optimize for risk control.

Combining both data models often leads to conflicting priorities.

These systems should remain logically separated.

Ignoring Portfolio Monitoring

Successful loan origination means little if repayment performance is not actively monitored.

Portfolio analytics must be treated as a core system component rather than an afterthought.

The Business Impact of a Lending OS

Organizations that implement structured lending workflows typically see measurable operational improvements:

- Faster underwriting cycles

- Improved portfolio risk visibility

- More consistent borrower communication

- Stronger financial forecasting accuracy

The system transforms commercial lending from a fragmented administrative process into a structured financial information system.

Final Architecture Summary

A complete Commercial Real Estate Lending OS generally contains:

- Deal acquisition pipeline

- Underwriting intelligence workspace

- Compliance monitoring layer

- Portfolio analytics dashboard

- Document control system

- Workflow automation infrastructure

Commercial lending is not simply the act of issuing loans.

It is the continuous management of financial risk across complex information systems.

For organizations building structured operational systems for financial workflows, SectorOps provides frameworks and operating system templates designed specifically for industries such as commercial real estate.

Learn more: